To find the perfect home or investment parcel in California whether tucked away in the scenic valleys of Sacramento, sitting near the coast in Orange County, or positioned alongside a peaceful river in Sonoma. The price is right, the location is ideal, and you are ready to remove your contingencies. But then, your lender drops a financial bombshell. The parcel sits directly inside a high risk 100 year floodplain, and you are legally required to buy expensive force placed insurance for thousands of dollars every year. California’s diverse geography makes it incredibly beautiful, but it also exposes properties to severe weather events, atmospheric rivers, and sudden flash flooding. If you skip running a proper California FEMA flood maps lookup before finalizing a real estate purchase or drafting construction plans, you risk inheriting an uninsurable asset or a property exposed to severe environmental hazards. Fortunately, the Federal Emergency Management Agency (FEMA) provides free, open access to its digital mapping databases. This step by step guide will teach you how to look up any California property’s flood risk, decode complex emergency management terms, and use official tools like a seasoned land professional.

What is a FEMA Flood Insurance Rate Map (FIRM)?

A flood insurance rate map (FIRM) is the official regulatory map produced by FEMA to highlight the specific geographic areas within a community that are subject to distinct levels of flood risk. Local planning commissions, insurance underwriters, and federal agencies rely on these specialized digital cartography frameworks to evaluate risk management profiles.

[Atmospheric Rivers / Storm Runoff] ──> FEMA Risk Assessment ──> FIRM Digital Mapping Data ──> Insurance Mandates

FEMA breaks these maps down into distinct regions known as a flood zone designation. These designations identify whether a piece of real estate sits in a low, moderate, or high risk grid. Knowing these letters helps you calculate risk and avoid unexpected development costs.

Decoding FEMA Flood Zone Designations in California

When you launch an official mapping portal, you will encounter various alphanumeric zones. Understanding these codes is essential for determining if a property faces structural or financial restrictions.

The table below breaks down the foundational FEMA flood zones used across California municipalities.

| Risk Level | Common Flood Zone Codes | Real Estate & Insurance Implications |

| High Risk (SFHA) | Zone A, AE, AH, AO, VE | Located inside the 100 year floodplain. Mandatory flood insurance is required for all federally backed mortgages. |

| Moderate Risk | Zone X (Shaded), Zone B | Located inside the 500 year floodplain. Insurance is highly recommended but not legally mandated by federal lenders. |

| Minimal Risk | Zone X (Unshaded), Zone C | Outside the high risk flood boundaries. Standard local insurance rates apply, and flood risks are considered historically low. |

The Critical Special Flood Hazard Area (SFHA)

If your California FEMA flood maps lookup reveals that your property falls within Zones A or V, your parcel is officially located inside a Special Flood Hazard Area (SFHA). Properties inside an SFHA have a 1% annual chance of experiencing a major flood event. Over the lifespan of a standard 30 year home mortgage, that translates to a staggering 26% cumulative chance of suffering severe structural water damage. Because of this high statistical exposure, the National Flood Insurance Act places strict legal requirements on these properties.

Understanding Base Flood Elevation (BFE)

For properties sitting within high risk zones, professional developers and structural engineers look closely at a metric known as base flood elevation (BFE). The BFE represents the official computed height to which floodwaters are statistically anticipated to rise during a base flood event (the 1% annual chance flood). It is calculated using advanced hydraulic engineering formulas.

Structural Safety Margin = Finished Floor Elevation of Building – Base Flood Elevation (BFE

If you plan to build a new home, an Accessory Dwelling Unit (ADU), or a commercial asset inside an SFHA, local California building codes require that your building’s lowest finished floor sit at or above the established BFE. Building below this level can lead to a denial of occupancy permits and exponentially higher insurance premiums.

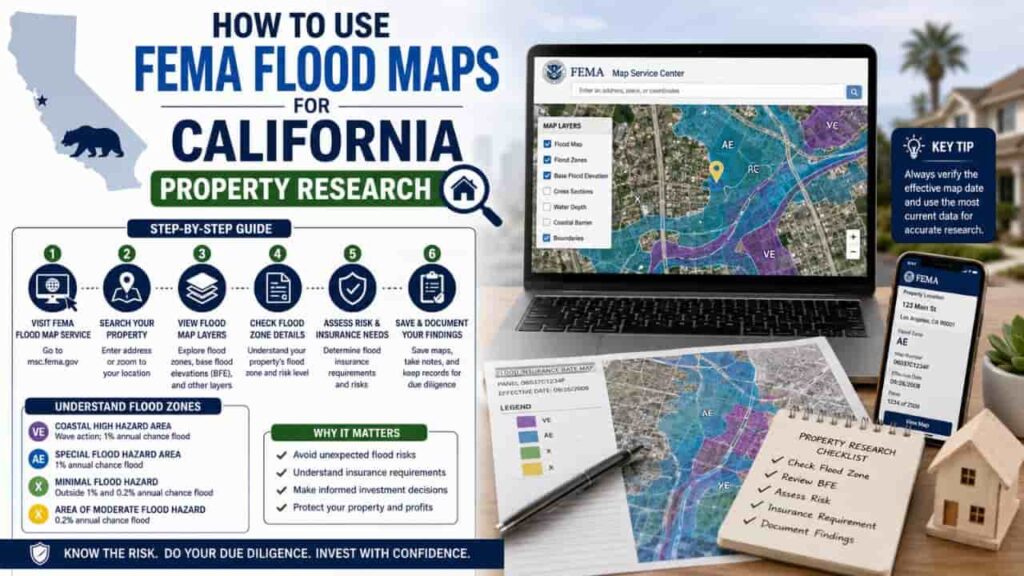

Step by Step Guide, How to Run a California FEMA Flood Maps Lookup

Ready to check a property’s risk profile? Follow this official step by step process to run your due diligence like a real estate expert.

Step 1. Access the Official FEMA Flood Map Service Center

Go directly to the official government portal at the FEMA Flood Map Service Center (MSC). Avoid third party real estate blogs, as their downloaded graphics may lack recent community map revisions.

Step 2. Input the Target Property Address Details

Type the exact street address, city, and ZIP code into the central search input box. Press enter to let the digital mapping engine locate your target parcel grid.

Step 3. Analyze the Interactive Flood Boundaries

Look at the visual map overlay centered on your lot lines. Identify if your lot is covered by dark blue pixel screens (High Risk SFHA) or lighter shaded patterns (Moderate Risk).

Step 4. Generate an Official FIRMette Map File

Click on the “Print MAP / FIRMette” utility button on the left panel. The portal will generate a customized, legally recognized excerpt of the larger map centered on your property. Save this file for your lenders and insurance agents.

Step 5. Verify the Base Flood Elevation Values

If your lot sits inside an “AE” zone, look closely for the static wavy lines crossing the map. The number printed next to these lines reveals the exact BFE value (in feet) for your parcel.

The FIRMette Tool and Mandatory Insurance Requirements

The FEMA FIRMette tool is a valuable resource for anyone researching real estate. A FIRMette is a full scale, digitized copy of an official flood insurance rate map (FIRM) formatted to print easily on standard office paper. Because it contains all official map headers, panel dates, and community numbers, it serves as a legally binding document. Title companies, mortgage underwriters, and real estate attorneys accept a certified FIRMette as official proof of a property’s flood status.

Federal Purchase Mandates

If your FIRMette reveals that a property falls within an SFHA, and you secure a mortgage through a federally regulated lender (like Chase, Wells Fargo, or any loan backed by Fannie Mae or Freddie Mac), you face mandatory flood insurance purchase requirements. You cannot waive this coverage. Failing to maintain an active flood policy can cause your lender to default your loan or force place a costly insurance policy at your expense.

Key Takeaways

Completing a California FEMA flood maps lookup is an essential piece of real estate due diligence. By learning how to use the Flood Map Service Center, print official FIRMettes, and identify your specific flood zone designation, you can protect yourself from unexpected insurance expenses and severe structural hazards. Never rely on guesswork, always verify your data through official federal channels to ensure your property investments remain safe, dry, and financially secure.

FAQs

What does it mean if my property is inside a 100 year floodplain?

It means the area has a 1% statistical chance of flooding in any given year. This adds up to a 26% cumulative risk of flood damage over a standard 30 year mortgage.

Can a standard home insurance policy cover flood damage in California?

No. Standard California homeowners insurance policies completely exclude water damage caused by rising outdoor waters, mudflows, or surface water runoff.

What is the FEMA FIRMette tool used for?

The FIRMette tool lets users print a legally recognized, small scale excerpt of an official federal flood map directly from their home computer.

How can I remove my home from a high risk flood zone designation?

If you believe your property was placed in an SFHA by mistake, you can hire a surveyor to submit physical elevation data to FEMA to request a formal Letter of Map Amendment (LOMA).

Are 500 year flood zones required to buy flood insurance?

No. Shaded Zone X properties (500 year floodplains) are not legally forced by federal lenders to carry insurance, though buying a policy is still highly recommended.

Where do I find the official Base Flood Elevation (BFE) for my lot?

You can find the BFE value printed on a property’s official flood insurance rate map (FIRM), usually shown as a number next to wavy lines within Zone AE grids.

What is an atmospheric river’s impact on California flood maps?

Atmospheric rivers dump massive volumes of rainwater over short windows, causing local infrastructure systems to overflow and expanding the real world boundaries of local flood basins

Does a grandfathered flood insurance rate change when a home is sold?

Under FEMA’s updated Risk Rating 2.0 system, insurance rates are calculated based on individual structural risks rather than historical policy grandfathering tiers.

Can I build an addition on a home located inside an SFHA?

Yes, but your local building department will require the new addition’s foundation and living spaces to be elevated to match or exceed the area’s current BFE.

How often does FEMA update its California flood maps?

FEMA updates maps incrementally as regional typography changes, flood control infrastructure is built, or new engineering studies are completed by local water districts.