Selling real estate in California involves a clear calculation of closing expenses, where the state’s real estate transfer tax (Closing Cost) directly impacts your net proceeds. Unlike states using a simple flat fee, California applies a multi-tiered system combining a baseline documentary transfer tax with localized city levies. Understanding who handles this cost, how county recorder schedules calculate the base rate, and where additional municipal taxes apply is essential for accurate financial forecasting.

1. The Core Components of California Transfer Taxes (Closing Cost)

When real property is sold and a new deed is recorded, government entities levy a tax for documenting the transfer of ownership. This property transfer cost is broken down into two potential layers:

County Documentary Transfer Tax to Closing Cost

Authorized by California Revenue and Taxation Code Section 11911, every county in California charges a baseline tax rate of $1.10 per $1,000 of the property’s final sale value (often calculated as $0.55 per $500). This baseline applies universally across all 58 counties.

City Transfer Tax

Certain municipalities specifically “charter cities” exercise their legal authority to levy an additional city transfer tax on top of the county rate. These rates vary dramatically by location. If a property sits within an incorporated city that does not have its own transfer tax, only the standard county rate applies.

2. Who Pays the Transfer Tax in California?

The allocation of transfer taxes is completely negotiable between the buyer and the seller, and it is explicitly written into the California Residential Purchase Agreement (RPA). However, regional market customs dictate the default expectations at escrow:

- Southern California (e.g., Los Angeles, Orange, San Diego Counties):

Customarily, the seller pays both the county and city transfer taxes as part of their standard closing expenses. - Northern California (e.g., Bay Area, Santa Clara, San Francisco):

Customarily, the buyer pays the transfer taxes, or the costs are split 50/50 between both parties. - Central Valley & Inlands:

Customs vary by county; splits are frequently negotiated depending on whether it is a buyer’s or seller’s market.

3. Standard County vs. Charter City Rates

To accurately estimate your closing expenses, you must know both the county and city jurisdictions governing the parcel. The following three-column table outlines the total combined real estate transfer tax California rates across major real estate markets, reflecting standard baseline rates alongside localized charter city rules:

| Municipal Jurisdiction | Combined Tax Rate (Per $1,000 of Value) | Primary Responsible Party (By Custom) |

| Standard CA County (Unincorporated or Non Charter) | $1.10 | Varies by Regional Custom |

| San Francisco (City & County Combined) | $5.00 to $60.00 (Tiered by Value) | Negotiable (Often split or paid by Buyer) |

| San Jose | $4.40 to $19.40 (Tiered by Value) | Buyer Customary |

| Oakland | $11.10 to $26.10 (Tiered by Value) | Seller Customary |

| Berkeley | $16.10 to $26.10 (Tiered by Value) | Buyer Customary |

| Sacramento | $3.85 | Seller Customary |

| Los Angeles (City Limits) | $5.60 to $61.60 (Subject to Measure ULA) | Seller Customary |

4. Step by Step Calculation for Standard Transactions

For properties located outside of high tax charter cities, calculating the standard documentary transfer tax and county recorder fee is a straightforward mathematical process.

Step 1: Determine the Taxable Value

The tax is calculated based on the “consideration” paid for the property, minus any liens or encumbrances remaining on the property at the time of sale (such as an assumed mortgage). If the property sells for $850,000 with no assumed loans, the taxable value is $850,000.

Step 2: Apply the Baseline Formula

Divide the total taxable value by $1,000 and multiply by the standard county rate of $1.10.

Transfer Tax = $Property Value/$1,000 x $1.10

Step 3: Rounding Up

California law requires rounding up any fractional amounts to the nearest tax bracket increment ($500 or $1,000 depending on county guidelines) before final calculation.

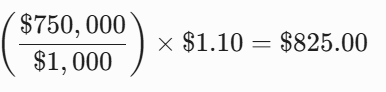

Example Calculation:

For a property in an area with only the standard county tax sold for $750,000:

$750,000\$1,000 x $1.10 = $825.00

The baseline property transfer cost for this transaction is exactly $825.00.

5. High Value “Mansion Tax” Cliffs: Los Angeles & Beyond

Sellers of luxury real estate or commercial assets must account for localized, progressive tax structures that create steep cost brackets based on valuation thresholds.

Los Angeles City Limit Transactions & Measure ULA

Properties within the boundaries of the City of Los Angeles are subject to Measure ULA (the Homelessness and Housing Solutions Tax). This is a gross-value transfer tax, meaning it is calculated on the total sale price from dollar one, regardless of existing mortgages or net profits.

- Sales under $5,300,000: The city base rate is $4.50 per $1,000, plus the county’s $1.10, totaling $5.60 per $1,000.

- Sales from $5,300,000 to $10,600,000: An additional 4.0% tax is levied, bringing the combined rate to 4.45% plus the county baseline.

- Sales of $10,600,000 or greater: An additional 5.5% tax applies, pushing the combined city and county rate to 5.95%.

These thresholds create extreme financial “cliffs.” For instance, a sale at exactly $5,300,000 triggers no ULA tax. A sale at $5,300,001 triggers an immediate 4% tax on the entire amount, resulting in over $212,000 in additional closing expenses.

6. Common Legal Exemptions to Transfer Taxes

Not every change in property ownership requires paying a documentary transfer tax. The state of California outlines several strict legal exemptions where a transfer can occur tax-free:

- Interspousal Transfers:

Transfers of property between spouses or registered domestic partners during a marriage, or as part of a formal divorce settlement agreement. - Gifts and Inheritances:

Properties transferred as a gift or through a will/estate planning vehicle where no monetary consideration or debt payoff is exchanged. - Living Trusts:

Transferring titles into a revocable or irrevocable living trust where the proportional ownership interests remain identical. - Foreclosures:

Deeds given to a beneficiary or mortgagee in lieu of a foreclosure proceeding, up to the value of the outstanding debt.

To claim these exemptions, the specific Revenue and Taxation Code section must be cited explicitly on the face of the Document Transfer Tax Declaration form submitted to the county recorder.

7. Strategic Solutions for Managing Closing Expenses

Minimizing transaction friction requires strategic preparation well before escrow documents are finalized:

- Verify Exact Municipal Boundaries:

Look up the exact parcel via the county geographic information system (GIS) mapping portal. A property may have an “Los Angeles” mailing address but actually reside within an unincorporated county area or a separate city like Beverly Hills, completely bypassing Measure ULA. - Factor Transfer Taxes into the Net Sheet:

Always request a preliminary seller’s or buyer’s net sheet from your title officer to model specific net return scenarios before accepting an offer. - Negotiate Purchase Price vs. Concessions:

If a transaction sits near a progressive tax cliff (e.g., $5.3 million in LA), negotiating concessions or structural property terms to keep the gross contract price below the threshold can save hundreds of thousands of dollars legally.

Conclusion

The shifting landscape of California property tax regulations requires authoritative insight, especially with the upcoming November 2026 ballot challenges to Los Angeles Measure ULA. While the current 2026 inflation-adjusted ULA tax thresholds demand strategic planning for high-value commercial and residential real estate transactions, executing a legal 1031 exchange remains a highly effective method to defer capital gains tax liabilities. Maximizing your financial returns hinges on understanding municipal exemptions, county auditor guidelines, and local assessment structures. Partnering with a certified specialist ensures compliance, protects your equity, and mitigates overall real estate transfer tax exposure.

FAQs

What is the current Los Angeles Measure ULA threshold for 2026?

As of 2026, the inflation-adjusted Measure ULA thresholds trigger a 4% transfer tax on sales over $5.3 million and a 5.5% tax on transactions hitting $10.6 million or more.

Does the LA mansion tax apply to commercial real estate?

Yes. Despite its popular “mansion tax” nickname, Measure ULA applies broadly to all commercial properties, multi-family apartment buildings, industrial assets, and vacant land within Los Angeles city limits.

How can property owners legally avoid the Measure ULA tax?

Sellers can minimize exposure by utilizing a 1031 exchange to defer taxes, transferring assets to qualified affordable housing nonprofits, or selling structured parcels below the $5.3 million threshold.

Is there a 2026 ballot initiative to repeal Measure ULA?

Yes. The California Taxpayer Protection Act has officially qualified for the November 3, 2026 statewide ballot, which seeks to cap municipal real estate transfer taxes at 0.05%.

Who is legally responsible for paying the ULA transfer tax?

The seller is legally responsible for paying the additional ULA transfer tax at the close of escrow, calculated based on the gross property sale price, not net equity.

Are mixed use property developments exempt from the LA mansion tax?

Currently, no. However, city council proposals are actively being debated in 2026 to create a 15-year ULA tax exemption specifically for new multi-family and mixed-use construction projects.

How does a 1031 exchange interact with real estate transfer taxes?

While a standard 1031 exchange successfully defers federal and state capital gains tax liabilities, it does not automatically exempt the seller from local municipal documentary transfer taxes like ULA.

Does Measure ULA apply to properties in Beverly Hills or Malibu?

No. Measure ULA only applies strictly to properties located within Los Angeles city boundaries. Incorporated cities like Beverly Hills, Santa Monica, and Malibu are completely exempt from this tax.

How often do California property tax thresholds adjust for inflation?

The Los Angeles Office of Finance adjusts the ULA tax brackets annually on July 1st, utilizing data from the Bureau of Labor Statistics Chained Consumer Price Index.

Where can I find official GIS mapping and county auditor records?

You can access verified parcel data, tax histories, and GIS mapping boundaries directly via your local County Auditor-Controller or City Office of Finance online portal.