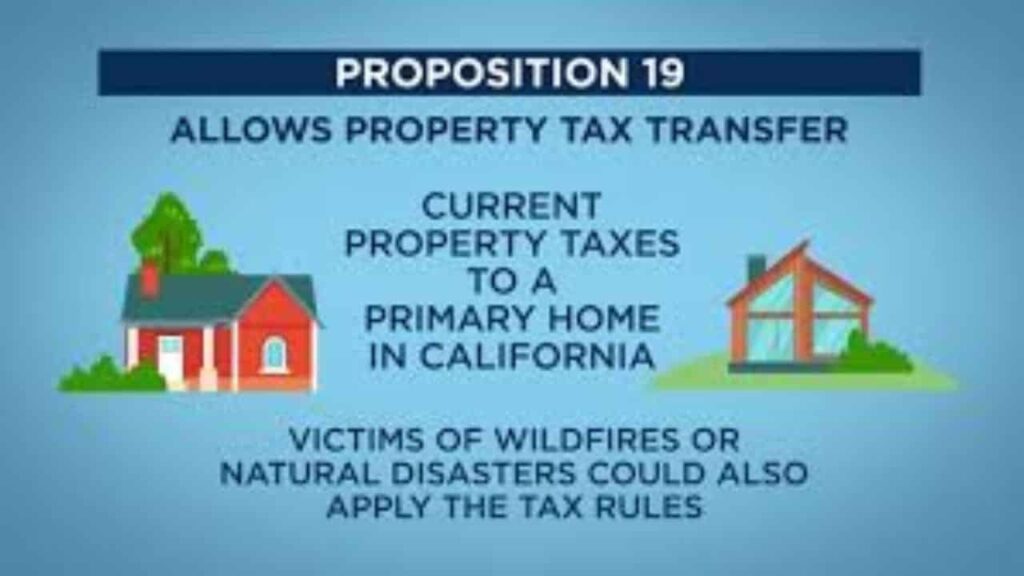

Passed by voters as the “Home Protection for Seniors, Severely Disabled, Families, and Victims of Wildfire or Natural Disasters Act,” Proposition 19 fundamentally reshaped the landscape of California real estate taxation. Implementing structural updates that took full effect in 2021, this constitutional amendment offers historic portability advantages for specific demographics while simultaneously dismantling long standing generational wealth tax shelters. As an expert digital real estate analyst and tax framework strategist, I have developed this comprehensive guide to help you, the intricacies of a California Proposition 19 property tax adjustment. Whether you are seeking a tax base transfer for retirement or attempting to decode the stringent new parent to child transfer rules, this authoritative walkthrough breaks down your statutory rights down to the dollar.

The Core Shifts, Goodbye Propositions 60, 90, and 58

To understand Proposition 19, one must first recognize what it replaced. For decades, older homeowners relied on Propositions 60 and 90 to freeze their assessed property values when downsizing, while families utilized Proposition 58 to pass real estate to heirs without triggering a steep market value reassessment under Proposition 13.

The Old Safeguards vs The Current Reality

Under the historical framework, eligible residents could only transfer their tax base once in a lifetime, restricted heavily by county to county agreements (inter county reciprocity). Furthermore, inherited properties including secondary vacation homes and commercial rentals were completely exempt from reassessment up to an additional $1 million in assessed value, regardless of how the heirs used them.

Proposition 19 completely erased those old boundaries. It launched a highly dynamic statewide portability structure for seniors while severely tightening the tax rules for inherited property tax exclusions.

1. Portability Rules, Over 55 Tax Relief & Disaster Victims

For qualifying individuals, Proposition 19 provides unprecedented flexibility to relocate anywhere within the State of California without facing a property tax penalty.

Who Qualifies for Base Year Value Portability?

The portability benefits of Prop 19 apply exclusively to three distinct groups of primary homeowners.

- Seniors

Homeowners who are over 55 years of age at the time of the original property sale. - Severely Disabled Individuals

Homeowners with permanent physical or mental disabilities. - Wildfire & Disaster Victims

Homeowners whose primary residences sustained greater than 50% damage in a Governor declared state of emergency.

Expanded Lifetime Limits and Values

Eligible claimants can now execute a base year tax transfer up to three times over their lifetime (and indefinitely for disaster victims), a massive upgrade from the historical single use constraint. Crucially, you are no longer restricted to purchasing a replacement home of “equal or lesser value.” You can purchase a more expensive property anywhere in California; however, a specialized mathematical adjustment will add the market value differential onto your original tax base.

| Prop 19 Portability Criteria | Previous Law (Props 60 / 90) | Current Law (Proposition 19) |

| Geographic Boundary | Limited to participating counties | Valid across all 58 CA counties |

| Lifetime Allocation | Allowed strictly once per lifetime | Allowed up to three times per person |

| Replacement Value Cap | Must be of equal or lesser value | Any market value allowed (with adjustments) |

2. Step by Step Portability Calculation, Buying a More Expensive Home

If you utilize the over 55 tax relief provision to purchase a replacement home that costs more than the original property you sold, the California State Board of Equalization (BOE) applies a strict blended tax rate formula.

New Taxable Value = Original Factored Base Year Value + Replacement Home Market Value – Original Home Sale Price

1.Execute the Original Sale and Purchase, Within 2 Years.

You must sell your original primary residence and buy (or complete new construction on) your replacement primary residence within a strict two year window of each other.

2.Calculate the Value Differential, BOE Math Formula.

Suppose your original home sells for $800,000, carrying an old taxable base year value of $250,000. You purchase a downsized luxury condo in a premium market for $1,000,000. The market difference is exactly $200,000 ($1,000,000 minus $800,000).

3.Determine the Adjusted Base Value, Blending the Assessment.

The county assessor takes your original tax base ($250,000) and adds the market value difference ($200,000). Your brand new, adjusted taxable base year value becomes $450,000, shielding you from being taxed at the full $1,000,000 purchase price.

4.Submit Form BOE 19 B, 3 Year Filing Window.

File your formal transfer claim with the local county assessor where the new home is located. You have three years from the date of purchase to file for retroactive tax refunds back to your move in date.

3. The New Intergenerational Rules, Parent to Child Transfers

While Prop 19 expanded rights for seniors, it concurrently introduced some of the most aggressive restrictions on inherited real estate in California history.

The Death of the Rental Property Loophole

Under current parent to child transfer rules, all secondary properties, commercial assets, and non primary vacation homes are 100% fully reassessed to fair market value upon transfer or inheritance. There are zero exemptions available for these property types.

Primary Residence Occupancy Mandate

For a child to successfully inherit a parent’s low property tax base, the home must have been the parent’s primary residence, and the inheriting child must move into the property as their primary residence within one year of the transfer date. Furthermore, the child must file for a Homeowners’ Exemption (Form BOE 266) within that exact same 12 month window. If the child ever moves out and converts the family home into a rental asset later in life, the tax exclusion is instantly revoked, and the home is reassessed to full market value.

The $1 Million Value Cap Limitation

Even if the child fulfills the occupancy mandate, the tax exclusion is capped. The law allows the child to absorb the parent’s old taxable value plus a statutory threshold of $1 million (which is indexed upward every two years for inflation; for recent cycles, it sits at $1,044,586). If the current fair market value of the home exceeds this combined threshold, the excess value is added directly to the property’s new tax bill.

Summary of Key Takeaways

Maximizing the California Proposition 19 property tax benefits requires strict adherence to statutory deadlines and occupancy mandates. Eligible seniors over 55 and disaster victims must finalize their replacement home purchase within a rigorous two year window to successfully secure a tax base transfer across county lines. Concurrently, search the updated parent to child transfer rules demands that inheriting heirs claim the primary residence exemption within 12 months. By managing this transition strategically, families can protect generational equity and avoid full market reassessments under California’s evolving inherited property tax framework.

FAQs

Can I transfer my California property tax base to another state?

No. Proposition 19 is a California constitutional amendment. The tax base transfer is strictly internal and applies only to replacement homes bought within the state’s 58 counties.

Do both spouses need to be over 55 to claim Prop 19 tax relief?

No. Only one spouse listed on the title must be at least 55 years old at the time the original primary residence is sold to qualify for the transfer.

What happens if I buy my new home before I sell my old one?

Prop 19 accommodates this completely. You have a full two year window. If you buy your replacement home first, you have exactly 24 months from that purchase date to sell your original home and claim your tax base adjustment.

Can grandchildren qualify for the intergenerational exclusion under Prop 19?

Yes, but only under narrow conditions. Grandchildren qualify for the transfer exclusion only if all parents of that grandchild who qualify as the children of the grandparents are deceased on the exact date of the property transfer.

What form do I file to transfer my tax base as a senior?

You must request and complete Form BOE 19 B (“Claim for Transfer of Base Year Value to Replacement Primary Residence”) from the county assessor’s office where your new property is located.

If multiple children inherit a family home, do all of them have to move in?

No. To maintain the parent child exclusion, only one of the inheriting siblings needs to establish the home as their primary residence and file the required homeowners’ exemption.

Does an inherited home stay excluded from tax reassessment forever?

Only as long as the eligible child continues to occupy the property as their primary residence into perpetuity. The moment the home is vacated or converted into a secondary asset, it undergoes full market reassessment.

How long do I have to file a parent to child exclusion claim?

To receive full retroactive tax relief from the date of the transfer or death, you must file Form BOE 19 P and your homeowners’ exemption within one year of the property transfer date.

What happens if an inherited home’s value is over the Prop 19 cap?

The value exceeding the parent’s taxable base plus the inflation adjusted $1 million cap is added directly onto the old tax base, resulting in a partial property tax increase rather than a full market reassessment.

Can a property held in a living trust qualify for Prop 19 base transfers?

Yes. Real estate held within a trust qualifies for both portability and intergenerational transfers, provided the claimants possess the present beneficial ownership interest in the asset.